Exhibit 99.1

Nasdaq: Common stock RNVA Warrants (July 2021) RNVAZ Diagnostics and Supportive Software Solutions to Healthcare Providers July 2017

This presentation includes forward - looking statements about Rennova Health’s anticipated results that involve risks and uncertainties . Some of the information contained in this presentation, including statements as to industry trends and plans, objectives, expectations and strategy for the business, contains forward - looking statements that are subject to risks and uncertainties that could cause actual results or events to differ materially from those expressed or implied by such forward - looking statements . Any statements that are not statements of historical fact are forward - looking statements . When used, the words "believe," "plan," "intend," "anticipate," "target," "estimate," "expect" and the like, and/or future tense or conditional constructions ("will," "may," "could," "should," etc . ), or similar expressions, identify certain of these forward - looking statements . Important factors which could cause actual results to differ materially from those in the forward - looking statements are detailed in filings made by Rennova Health with the Securities and Exchange Commission . Rennova Health undertakes no obligation to update or revise any such forward - looking statements to reflect subsequent events or circumstances, except to the extent required by applicable law or regulation . Note : This presentation includes certain “Non - GAAP” financial measures as defined by SEC rules . As required by the SEC, we have provided a reconciliation of those measures to the most directly comparable GAAP measures on the Regulation G slide included as slide 13 of this presentation . Non - GAAP financial measures should be considered in addition to, but not as a substitute for, reported GAAP results . Forward Looking Statements and Non - GAAP Information 2

We are Rennova Health 3 Healthcare is Being Transformed

• Five - year history of operations in clinical laboratory space • Toxicology • Clinical • Genetic testing including pharmacogenomics and oncology • Three years in software development for the medical sector • Proprietary lab ordering and reporting • Lab information systems • Electronic Health Records • Medical billing software (Licensed) • Capital investment in our Clinical Labs of approximately $ 8 M • Own Labs in Florida, New Mexico, New Jersey, California and Connecticut • Adequate capacity to facilitate growth without additional investment • Investment in our Software assets of approximately $ 12 M • We operate in a very sizable and well established market place and offer products and services for which there is an increasing demand • We have a focused strategy for growth expanding from an historical concentration on servicing the substance abuse sector in Florida to a national and diverse marketplace to include the substance abuse and pain management sectors . • We have ; • A capable, experienced management team • Value added software products launched to create a sustainable relationship with contracted, recurring revenue • We have significant opportunity for growth of diagnostics revenues in 2017 and beyond leveraging our capability, our compliance record, expanded national footprint, our expanding menu of diagnostics and a rapidly increasing number of in - network contracts with a number of payers and secondary networks nationwide 4 Key Investment Highlights

• The diagnostics sector has changed dramatically in the last few years • Paper records and faxes meant different vendors to a medical provider could function side by side without communication • Electronic platforms and integration have created a need for providers of solutions to communicate efficiently, accurately, automatically and fast • Medical providers need more than just diagnostics; they need an increasing number of integrated and interoperable solutions to enable their business to function • Compliance needs have increased with an ever more demanding regulatory and payer environment • The need to have contracts with insurance companies and other payers to ensure receipt of payment for services is increasing Rennova has positioned itself to maintain a sustainable long term relationship with medical providers by providing a number of essential products and services, creating efficiencies for the provider and benefiting from additional contracted and recurring revenue for the provision of these services and products 5 Rennova Offers a Single Source Solution for Medical Providers

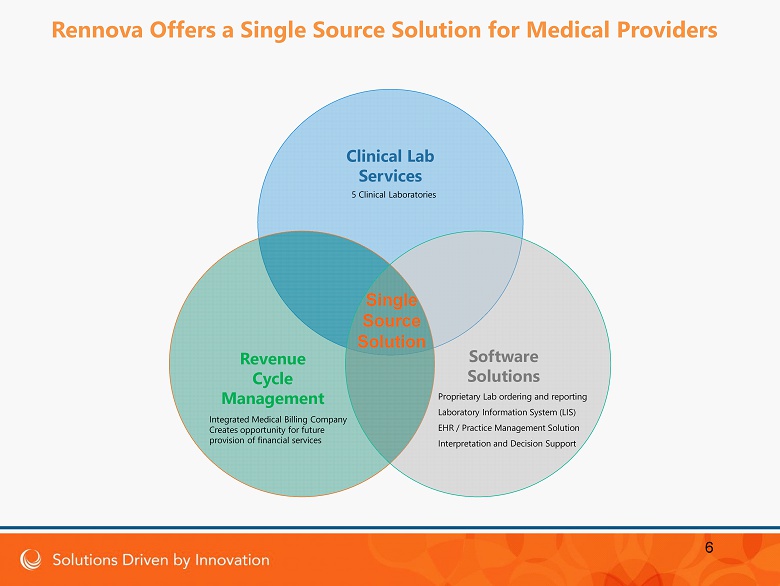

Clinical Lab S ervices Revenue Cycle Management Software S olutions Single Source Solution 5 Clinical Laboratories Integrated Medical Billing Company Creates opportunity for future provision of financial services Proprietary Lab ordering and reporting Laboratory Information System (LIS) EHR / Practice Management Solution Interpretation and Decision Support 6 Rennova Offers a Single Source Solution for Medical Providers

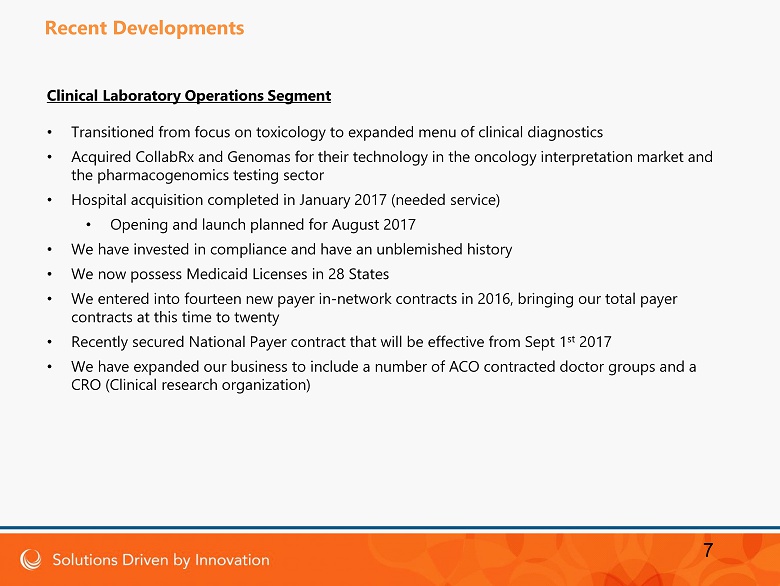

Clinical Laboratory Operations Segment • Transitioned from focus on toxicology to expanded menu of clinical diagnostics • Acquired CollabRx and Genomas for their technology in the oncology interpretation market and the pharmacogenomics testing sector • Hospital acquisition completed in January 2017 (needed service) • Opening and launch planned for August 2017 • We have invested in c ompliance and have an unblemished history • We now possess Medicaid Licenses in 28 States • We entered into fourteen new payer in - network contracts in 2016, bringing our total payer contracts at this time to twenty • Recently secured National Payer contract that will be effective from Sept 1 st 2017 • We have expanded our business to include a number of ACO contracted doctor groups and a CRO (Clinical research organization) 7 Recent Developments

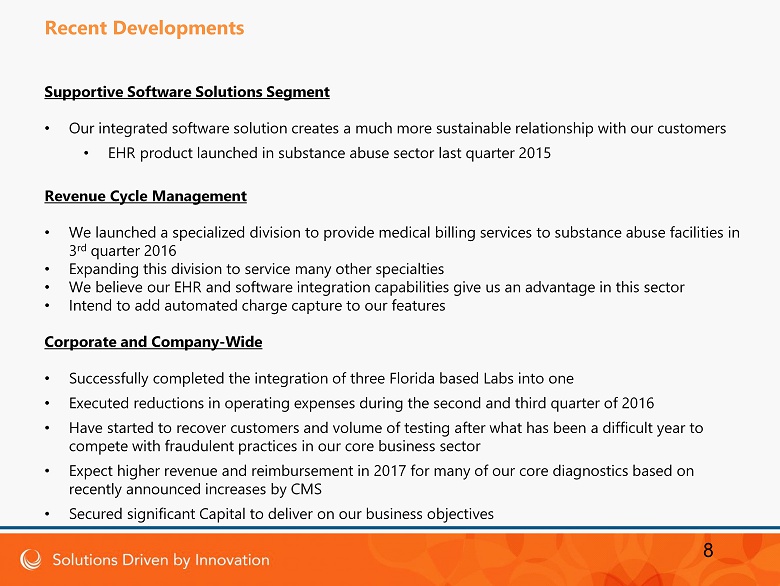

Supportive Software Solutions Segment • Our integrated software solution creates a much more sustainable relationship with our customers • EHR product launched in substance abuse sector last quarter 2015 Revenue Cycle Management • We launched a specialized division to provide medical billing services to substance abuse facilities in 3 rd quarter 2016 • Expanding this division to service many other specialties • We believe our EHR and software integration capabilities give us an advantage in this sector • Intend to add automated charge capture to our features Corporate and Company - Wide • Successfully completed the integration of three Florida based Labs into one • Executed reductions in operating expenses during the second and third quarter of 2016 • Have started to recover customers and volume of testing after what has been a difficult year to compete with fraudulent practices in our core business sector • Expect higher revenue and reimbursement in 2017 for many of our core diagnostics based on recently announced increases by CMS • Secured significant Capital to deliver on our business objectives 8 Recent Developments

Drug and Alcohol Rehabilitation • Total Market Size – estimated at $35 Billion* • Large and growing number of facilities in a fragmented market • Between 14,500 to 16,700 outpatient clinics* Market growth from high demand: • Over 23 million Americans are addicted to alcohol and other drugs** • The number of Americans in addiction treatment ranges from 2.5 million to 4.1 million*** • 3 to 5 million people who have a diagnostic addiction disorder warranting treatment will gain coverage through healthcare reform**** • Six states currently require some form of urine toxicology testing for the treatment of substance abuse or opioid therapy, and at least nine other states recommend such testing in their medical treatment guidelines Pain Management Sector • Total Market Size – estimated at $2 - $4 Billion***** • Large and growing number of clinics in a fragmented market • Private clinics in the U.S. estimated between 1,500 and 2,500******** • More than 6,800 doctors specialize in pain management and more than 600,000 doctors are licensed to prescribe pain medication********** Market growth from high demand: • Chronic pain affects an estimated 100 million Americans, or one - third of the U.S. population****** • Approximately 25 million people experience moderate to severe chronic pain with significant pain - related activity limitations and diminished quality of life***** • Between 5 to 8 million people use opioids for long - term pain management********* • In 2015, U.S. providers wrote 204 million prescriptions for opioid painkillers******* Market Drivers Lab Services Drivers • Secular growth • Compliance Value - added services • Efficiency • Cost • Revenue cycle management Sources: *IBIS World, **The National Council on Alcoholism and Drug Dependency , ***SAMHSA, **** National Association of Alcoholism and Drug Abuse Counselors ***** The U.S. Addiction Rehab Market, Bharat Publication, ******NIH, *******CDC and Pain Physician Publication . 9 Our Target Markets ******** U.S. Department of Justice and Federal Trade Commission, “Horizontal Merger Guidelines, August 2012, ********* National Institutes of Health “Pathways to Prevention Workshop: The Role of Opioids in the Treatment of Chronic Pain”, September 2014, ********** Champion Pain Care Corp 10 - K filing and t he U.S. Addiction Rehab Market, Bharat Publication

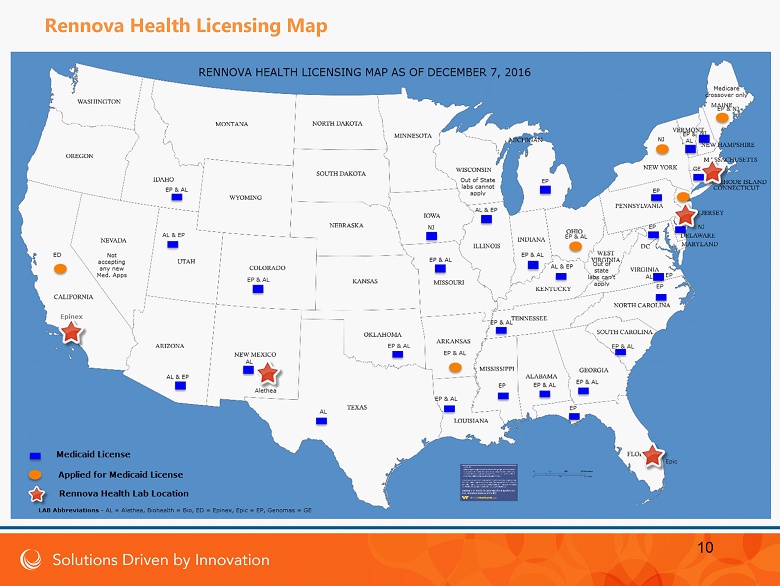

10 Rennova Health Licensing Map

• Initiated Medicaid Licensing & Third Party Payer Initiative in December 2015 o Applied for Medicaid Licenses in 34 States o We possess Medicaid Licenses in 28 States • Current Third Party Insurance Payer Contracts o Blue Shield of California o Coventry (National Contract) o Corvel o Multiplan o PrimeHealth o FedMed o HealthSmart o America’s Choice Provider Network o Tricare – South (Humana Military) o Health Net Services (Tricare North) o Three Rivers Provider Network o Fortified Provider Network o Galaxy Health Network o Passport Health Network (MCO Kentucky) o Wellcare (MCO Kentucky) o Stratose o Tricare – West (UHC) o Community Care Plan (MCO Florida) o Coventry Healthcare of Virginia (MCO Virginia) o McLaren Health Plan (MCO Michigan) 11 Our Payers

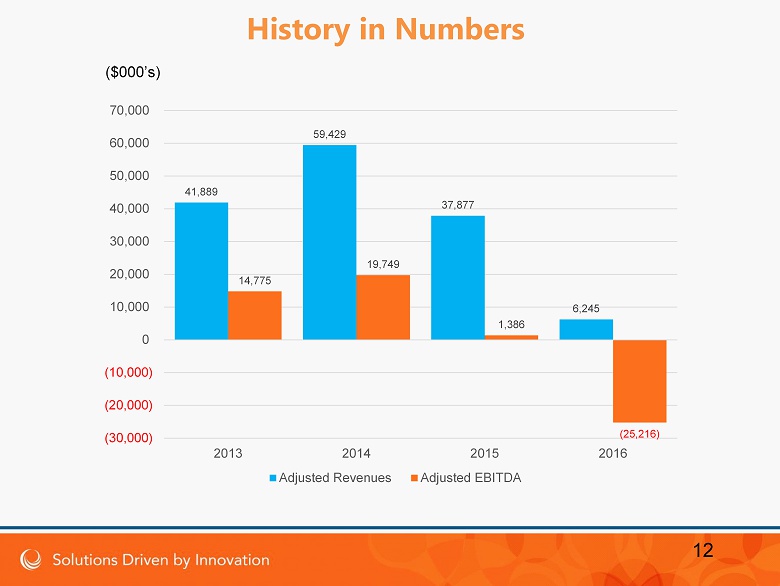

12 History in Numbers 41,889 59,429 37,877 6,245 14,775 19,749 1,386 (25,216) (30,000) (20,000) (10,000) 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 2013 2014 2015 2016 Adjusted Revenues Adjusted EBITDA ($000’s)

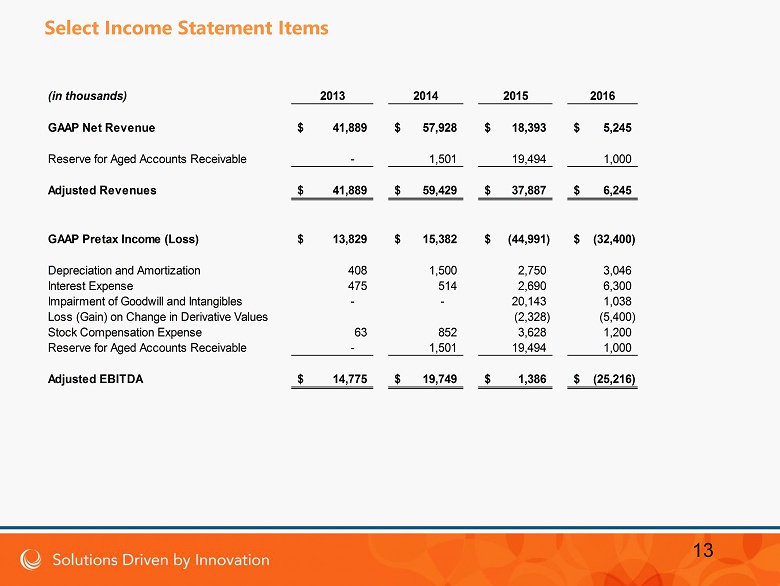

13 Select Income Statement Items (in thousands) 2013 2014 2015 2016 GAAP Net Revenue 41,889$ 57,928$ 18,393$ 5,245$ Reserve for Aged Accounts Receivable - 1,501 19,494 1,000 Adjusted Revenues 41,889$ 59,429$ 37,887$ 6,245$ GAAP Pretax Income (Loss) 13,829$ 15,382$ (44,991)$ (32,400)$ Depreciation and Amortization 408 1,500 2,750 3,046 Interest Expense 475 514 2,690 6,300 Impairment of Goodwill and Intangibles - - 20,143 1,038 Loss (Gain) on Change in Derivative Values (2,328) (5,400) Stock Compensation Expense 63 852 3,628 1,200 Reserve for Aged Accounts Receivable - 1,501 19,494 1,000 Adjusted EBITDA 14,775$ 19,749$ 1,386$ (25,216)$

Strategy 14

Create a sustainable relationship with our customers to grow recurring revenue and provide value to our shareholders How? Build from a toxicology - focused company to: 1. A significant and diverse diagnostics business including the provision of “needed services” from ownership of hospitals and Dr’s practices 2. Offering supportive software solutions that add value by generating sustainable customer relationships and revenue and then leveraging the integration and analytic capabilities to quickly assess value of receivables with an ambition to provide financial services 3. Exploring and developing new opportunities to improve provider and patient experiences and outcomes, including for diabetes and cancer diagnostics and products that are provided directly to patients . Remain proactive to the needs of patients and medical providers. 15 The Long Term Strategy

• Strengthen Core Diagnostic Business o Plan to o pen our 1 st hospital o Continue to capitalize on the disruption in toxicology sector o Increase Clinical testing o Grow Pharmacogenomics testing with Genomas o Launch DTC (Direct to Consumer) testing o Consider opportunities for acquisition of additional hospital and Dr’s practices • Accelerate Growth and/or Launch: o Software product sales o Medical Billing services as an integrated service o Interpretation and decision support in cancer diagnostics directly to doctors and public o Investigate opportunities for cancer diagnostics leveraging Genomas capabilities o Investigate opportunities for spin out of Genetic division and Software division 16 2017 Goals

• We believe that we ca n achieve the following revenues for 2018 o $600K per month for toxicology and clinical diagnostics o $400K per month for software and RCM related revenue o $1M per month from our hospital in TN Subject to acquisition o $800K per month from Dr’s practices o $1M per month from acquisition of additional hospital Potential revenue of $3.8M per month or $45.6M per annum 17 Our goal in numbers

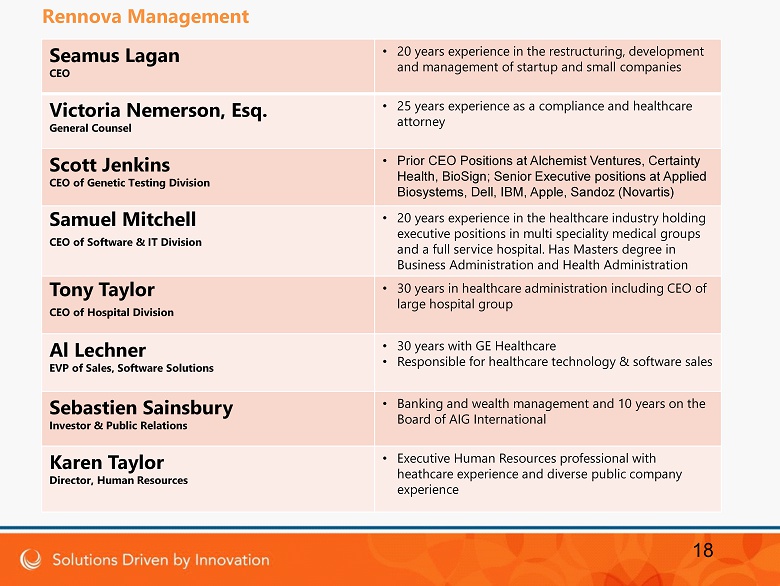

Seamus Lagan CEO • 20 years experience in the restructuring, development and management of startup and small companies Victoria Nemerson, Esq. General Counsel • 25 years experience as a compliance and healthcare attorney Scott Jenkins CEO of Genetic Testing Division • Prior CEO Positions at Alchemist Ventures, Certainty Health, BioSign ; Senior Executive positions at Applied Biosystems, Dell, IBM, Apple, Sandoz (Novartis) Samuel Mitchell CEO of Software & IT Division • 20 years experience in the healthcare industry holding executive positions in multi speciality medical groups and a full service hospital. Has Masters degree in Business Administration and Health Administration Tony Taylor CEO of Hospital Division • 30 years in healthcare administration including CEO of large hospital group Al Lechner EVP of Sales, Software Solutions • 30 years with GE Healthcare • Responsible for healthcare technology & software sales Sebastien Sainsbury Investor & Public Relations • Banking and wealth management and 10 years on the Board of AIG International Karen Taylor Director, Human Resources • Executive Human Resources professional with heathcare experience and diverse public company experience 18 Rennova Management

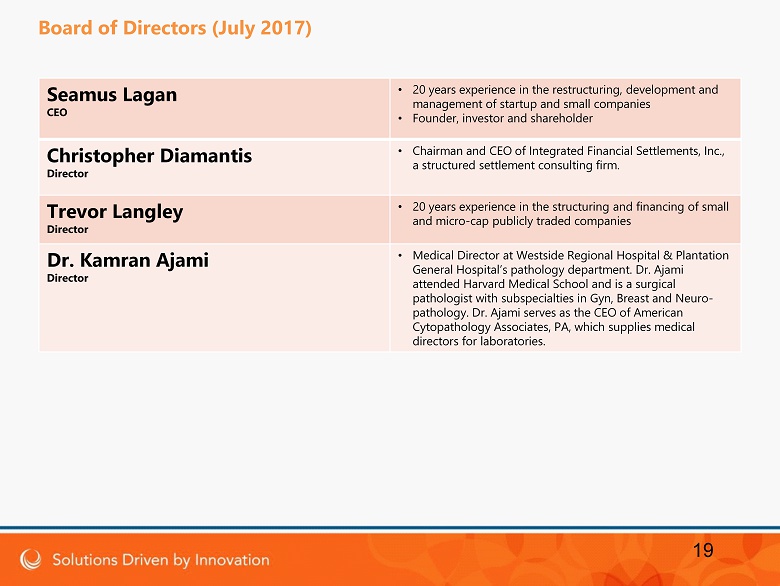

Seamus Lagan CEO • 20 years experience in the restructuring, development and management of startup and small companies • Founder, investor and shareholder Christopher Diamantis Director • Chairman and CEO of Integrated Financial Settlements, Inc., a structured settlement consulting firm. Trevor Langley Director • 20 years experience in the structuring and financing of small and micro - cap publicly traded companies Dr. Kamran Ajami Director • Medical Director at Westside Regional Hospital & Plantation General Hospital’s pathology department. Dr. Ajami attended Harvard Medical School and is a surgical pathologist with subspecialties in Gyn , Breast and Neuro - pathology. Dr. Ajami serves as the CEO of American Cytopathology Associates, PA, which supplies medical directors for laboratories. 19 Board of Directors (July 2017)

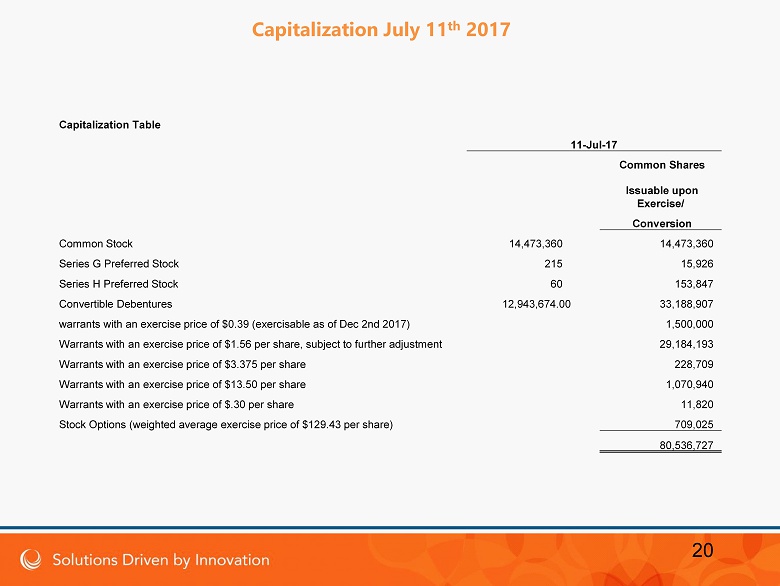

20 Capitalization Table 11 - Jul - 17 Common Shares Issuable upon Exercise/ Conversion Common Stock 13,908,360 13,908,360 Series G Preferred Stock 215 15,926 Series H Preferred Stock 60 153,847 Sabby Healthcare New Debenture 7,130,000 18,282,051 Sabby Bridge Exchange Debenture 2,464,500 6,319,231 Sabby Pref. H. Exchange Debenture - - Sabby Volatility Fund Debenture 2,223,132 5,700,339 Lincoln Park Debenture 1,155,856 2,963,734 Alpha Credit Pref.H. Exchange Debenture 190,576.14 488,657 warrants with an exercise price of $0.39 (exercisable as of Dec 2nd 2017) 1,500,000 Warrants with an exercise price of $1.56 per share, subject to further adjustment 29,184,193 Warrants with an exercise price of $3.375 per share 228,709 Warrants with an exercise price of $13.50 per share 1,070,940 Warrants with an exercise price of $.30 per share 11,820 Stock Options (weighted average exercise price of $129.43 per share) 709,025 80,536,832

• Five - year history of operations in clinical laboratory space • Toxicology • Clinical • Genetic testing including pharmacogenomics and oncology • Three years in software development for the medical sector • Proprietary lab ordering and reporting • Lab information systems • Electronic Health Records • Medical billing software (Licensed) • Capital investment in our Clinical Labs of approximately $ 8 M • Own Labs in Florida, New Mexico, New Jersey, California and Connecticut • Adequate capacity to facilitate growth without additional investment • Investment in our Software assets of approximately $ 12 M • We operate in a very sizable and well established market place and offer products and services for which there is an increasing demand • We have a focused strategy for growth expanding from an historical concentration on servicing the substance abuse sector in Florida to a national and diverse marketplace to include the substance abuse and pain management sectors . • We have ; • A capable, experienced management team • Value added software products launched to create a sustainable relationship with contracted, recurring revenue • We have significant opportunity for growth of diagnostics revenues in 2017 and beyond leveraging our capability, our compliance record, expanded national footprint, our expanding menu of diagnostics and a rapidly increasing number of in - network contracts with a number of payers and secondary networks nationwide 21 Key Investment Highlights